” The Institute for Fiscal Studies has stated that there has to be tax rises and these tax rises are going to be substantial.

We are not at the end of the Government spending yet because the pandemic is still with us.

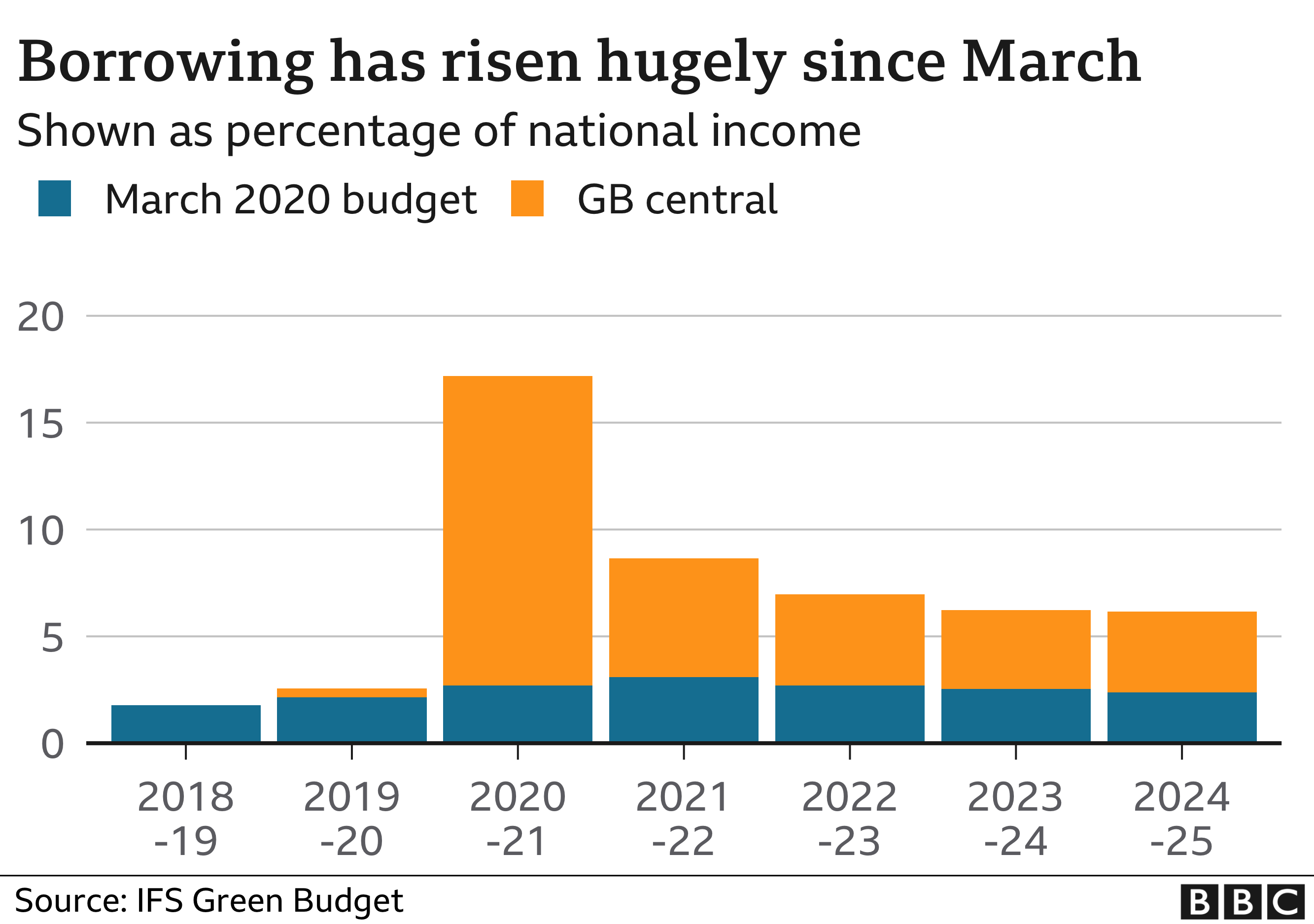

There has been a marked drop in Government spending recently with the ending of the Furlough scheme but the increase in borrowing since March has been staggering.

The borrowing has come from pension schemes, insurance companies and investors around the world.

Now is not a great time for tax rises but this looks inevitable. They may leave it until the middle years of the decade.”

Nigel Holland

Taxes rises of more than £40bn a year are ‘all but inevitable’ to protect UK government debt from spinning out of control, a think tank has warned.

The Institute for Fiscal Studies said borrowing this year will hit levels not seen in peacetime due to the pandemic.

It said the state had pumped an extra £200bn into the economy to support jobs, businesses and incomes this year.

This was necessary but would mean big tax hikes into the middle of the next decade, the IFS said.

To pay for the services it provides, the UK government borrows from pension funds, insurance companies and investors around the world, then tries to balance its books through taxes.

But in an update originally meant to accompany the chancellor’s now scrapped Autumn Budget, the IFS said this would become harder as the crisis rolled on.

It said the economy was forecast to be 5% smaller in 2024-25 than was projected back in March, which would leave the country with a £100bn hit to its finances from lower tax revenues.

At the same time, it said “higher borrowing will be with us for some time to come”.

The government will not, as the chancellor promised just a week ago, “always balance the books” and the Conservative manifesto commitment on lower debt is impossible, says the Institute for Fiscal Studies in its annual audit of the public finances.

Annual government borrowing this year will reach levels only previously reached during world wars, while the national debt will be bigger than the economy, reaching 110% of GDP by 2025.

However, the IFS warns that now is not the time for tax rises or spending cuts. The economy will continue to need support because of one of the worst pandemic hits to growth in the world, alongside the prospect of new post-Brexit trade barriers with the EU.

For now, extra borrowing is helped by extraordinarily low rates of interest paid by the government. But the IFS outlines a scenario where even significant tax rises, worth £40bn a year from the middle of this decade, will fail to get the size of the national debt below 100% of GDP.

Repaying the Covid support spending is, the institute suggests, going to be a delayed and then very gradual programme of tax-and-spend restraint that could last a generation.

Paul Johnson, director of the IFS, said the government had no choice but to ramp up spending in the short term, and there was little it could do “fully to protect the economy into the medium run”.

“We are heading for a significantly smaller economy than expected pre-Covid and probably higher spending too.

“Without action, debt – already at its highest level in more than half a century – would carry on rising. Tax rises, and big ones, look all but inevitable, though likely not until the middle years of this decade.”